One important part of financial analysis is comprehending the balance sheet. This article gives a picture of how much money a company has and what it owes at one specific moment in time. It is divided into two key parts: assets and liabilities, with shareholders' equity making things equal on both sides. In this article, we will discuss the balance sheet, looking closely at its different parts and understanding what they mean for a company's financial condition.

Overview of the Balance Sheet

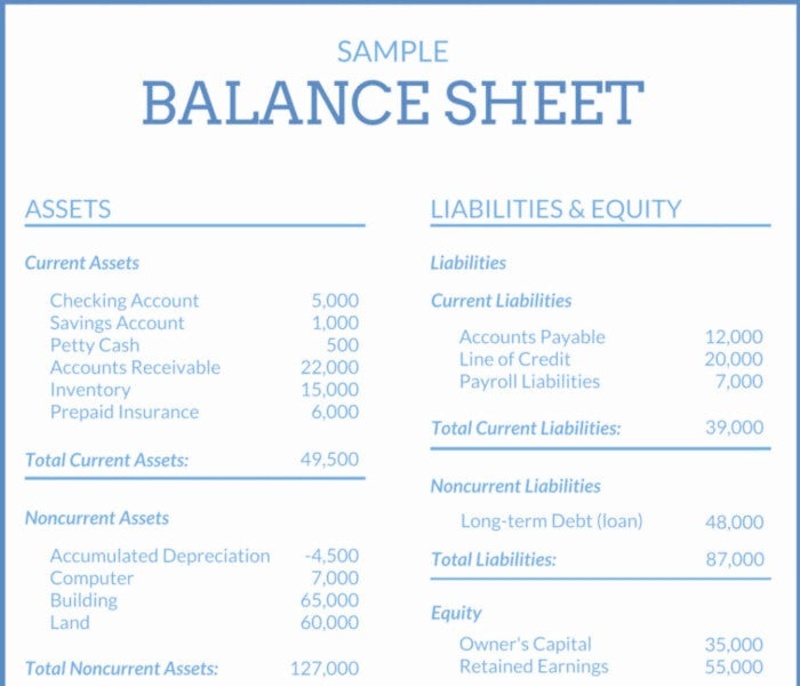

The balance sheet is an essential financial statement that shows a company's financial status by displaying its assets, liabilities, and shareholders' equity. Assets are what the company owns, liabilities represent what it owes to others, and shareholders' equity is the difference between these two, showing the net worth of the business. The balance sheet can help stakeholders understand how liquid or available cash flow a company has. If it's capable of paying off debts over time (solvency), as well as providing a general view of its monetary power.

The balance sheet is not just a fixed picture, it's also an active instrument for making decisions. It shows the financial condition at one time but can be used to predict future possibilities and help with strategy planning too. Stakeholders use this sheet to understand if the company can handle its short-term and long-term promises, see how it is set up in terms of capital structure, and measure its financial pressure.

- Transparency: The balance sheet provides transparency regarding a company's financial health, aiding investors in making informed decisions about investments.

- Comparative Analysis: Comparative analysis of balance sheets over different periods helps in identifying trends and patterns, facilitating better financial planning and management decisions.

Assets - The Building Blocks

An asset is a resource owned by the company, possessing economic value, and can be turned into cash. Usually, assets are divided into current ones and non-current ones. Assets that can be converted to cash within a year fall under the current category like money in hand, accounts that will receive payment soon from customers (accounts receivable), stock for selling purposes, or short-term investments among others. Assets not likely to be converted into cash within a year are known as non-current assets. These include long-term investments, property, plant and equipment (like buildings and machinery), as well as intangible assets such patents or copyrights that can give future economic advantages lasting more than one year.

The assets of a company are not only the physical properties it owns but also include intellectual properties like patents and trademarks. These contribute greatly to its competitive strength in the market. Knowing about what makes up these assets is very important when evaluating how much room for growth and innovation exists within an organization.

- Depreciation Impact: Non-current assets like property, plant, and equipment are subject to depreciation, impacting their valuation over time.

- Intangible Assets: Intangible assets, such as brand reputation and intellectual property, often play a critical role in determining a company's market value and competitive advantage.

Liabilities - The Obligations

Liabilities are the company's responsibilities or debts that need to be paid off in coming times, usually by transferring assets or providing services. They too have two kinds of assets, which are current and non-current. The ones falling under current liabilities refer to obligations that should be fulfilled within one year. These can include accounts payable, short-term loans, and accrued expenses among others. Moving away from current liabilities, non-current ones include long-term debt, deferred tax liabilities, and lease obligations that go beyond a year.

It is important to manage liabilities well to keep financial stability and endurance. Companies must find a good equilibrium between debt financing and equity financing to make their capital structure most efficient while lessening the danger in finance matters.

- Debt Covenants: Non-current liabilities often come with specific terms and conditions known as debt covenants, which companies must adhere to, impacting their financial flexibility and operational decisions.

- Interest Expense: Long-term debt obligations entail interest payments, which can significantly affect a company's profitability and cash flow.

Shareholders' Equity - The Ownership Stake

Shareholders' equity, also called net assets or net worth, shows the remaining interest in a company's assets after taking away liabilities. This is the amount of money that owners can claim on all the company's assets when they have paid off everything owed by their business. Shareholders' equity includes common stock, preferred stock, additional paid-in capital, retained earnings, and treasury stock. It acts as an indicator of the company's financial well-being and its capacity to create profits for its investors.

Shareholders' equity is not just a financial metric but also an indicator of investor confidence and trust in the company's management and prospects. Maintaining a healthy level of shareholders' equity is essential for attracting investment and sustaining business growth.

- Dividend Payments: Retained earnings, a component of shareholders' equity, are often used to finance growth initiatives or distributed to shareholders in the form of dividends, reflecting the company's capital allocation strategy.

- Stock Buybacks: Companies sometimes repurchase their shares as a means of returning capital to shareholders or signaling confidence in future performance.

Analyzing the Balance Sheet

When we study the balance sheet, we look at different financial ratios and metrics that come from its parts. Usually, these ratios include debt-to-equity ratio, current ratio, and return on equity along with other types of measurements. These give us useful information about how much money a company has available for use (liquidity), its amount of debt compared to what it owns (leverage), how well it uses assets to make money (efficiency), and finally the profit made about total ownership value or equity (profitability). Analysts can use these metrics to evaluate the company's performance by comparing them over time or against industry standards, which helps in making well-informed investment choices.

Besides financial ratios, techniques like horizontal and vertical analysis are used by analysts to make sense of balance sheet data. Horizontal analysis looks at financial information over many periods to find trends and alterations, while vertical analysis examines each line item as a part of a base figure - usually total assets or total liabilities. These tools of analysis help those with an interest in the company understand how important different parts are and what they mean for its overall financial situation.

- Financial Leverage: The debt-to-equity ratio measures the proportion of debt financing relative to equity financing, indicating the degree of financial leverage and risk exposure.

- Working Capital Management: The current ratio evaluates a company's ability to meet short-term obligations with its current assets, providing insights into its liquidity and operational efficiency.

Interpreting Changes Over Time

Changes in the balance sheet over time can reveal important trends and patterns in a company's financial condition. For instance, increasing assets and decreasing liabilities may indicate growth and improved financial health, while the opposite may signal financial distress. By conducting trend analysis and identifying key drivers behind these changes, stakeholders can better understand the underlying dynamics of the business and anticipate future performance.

Furthermore, comprehending why certain line items in the balance sheet change helps in making knowledgeable choices and tactical modifications. For instance, an upturn in accounts receivable could mean that sales are rising but it might also imply problems with customer payments or credit strategies. This necessitates more careful examination as well as proactive actions to deal with such matters.

- Seasonal Variations: Certain industries may experience seasonal fluctuations in business activities, leading to corresponding changes in their balance sheet metrics.

- Regulatory Compliance: Changes in accounting standards or regulatory requirements can impact the presentation and disclosure of financial information on the balance sheet, necessitating adjustments and updates to ensure compliance.

Conclusion

In conclusion, the balance sheet is a vital tool for understanding a company's financial position and assessing its overall health and stability. By examining its components, assets, liabilities, and shareholders' equity, along with relevant financial ratios, stakeholders can gain valuable insights into the company's operations, liquidity, solvency, and profitability. Regular analysis of the balance sheet enables investors, creditors, and management to make informed decisions and navigate the complexities of the financial markets.